In my blog a few weeks ago “Personal Finance Series 1 of X – Importance of checking your own credit and how to do it yourself”, I talked about how to pull your credit bureau for free and the reason why I recommend everyone to do it once a year, especially if you are planning to apply for mortgage in the foreseeable future. With new rules coming out from the government so frequently now there has never been a more important time to prepare your credit in best shape possible in order for the lender if give you the maximum amount of funds and at the lowest rate available.

Here is the link as a refresher:

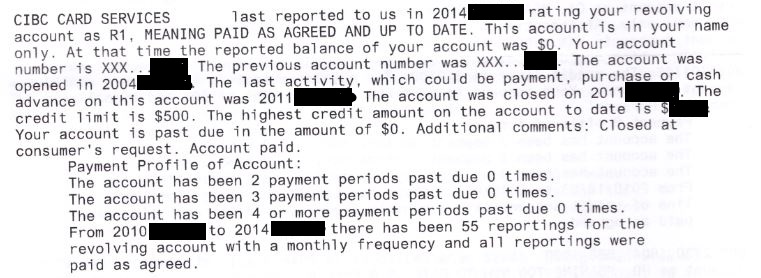

If you listened to my advise and pull the report, you should have received your report by now. Since I suspect most of you have never seen a credit report, I’ll show you here how a credit card will show on the report as an example.

This is more or less what your lender will see for each of your existing credit cards, line of credits, car loans, mortgages etc. In this case, this person had a CIBC credit card opened in 2010 with limit of $500. This card has since been closed in 2014 at consumer’s request. There are typically two types of closures: “by consumer” or “by credit grantor”. Your lender will view any facilities listed as “closed by credit grantor” with a red flag as usually there’s some issues with the account that leads of lender to initiate the closure. On the other hand, if you called in and close the credit facilities, like in this case, will be shown as “closed by consumer’s request”, and typically lender will not question that and deemed you no longer need it and wanted to be cancelled. Here you can see how many past due payments, in this case payments for the 55 months are all up to date. You will also noticed this card has “R1” status.

There are mostly 3 different types:

R – revolving account (ie credit card )

C – credit account (ie line of credits)

M – mortgage

And numbered between 0-9

0 – too new to rate (for facilities recently opened)

1- best rating possible

9 – worse rating possible

So when lender ask you how many credit cards you have and if they are paid on time, just keep in mind that they likely already know the answer before they ask you so you better off just tell the truth.

I am now offering 3 tips that will help you improve your first impression (credit wise) to you lender:

- review your report and call card companies to close any unused credit cards, especially those store credit cards that you have not been using for the past 10+ years that you weren’t even aware of. Remember, the less credit facilities you have, the faster the lender can process your application and the less complicated it is for them to review.

- if there is any “collection” item that is nominal amount, just call the company and pay it off. I know some of you will say it is the principal that matters, not the amount that you care about. Or you want to teach the company a lesson by not paying and let them go through the trouble of trying to collect from you. My advise is just pay it off. If you want to continue to compliant, go ahead after you have it paid. By not paying and shown as “collection” status on your report, you are in a position I refer to “win the battle but lost the war”. You might win the $25 from your TV/cellphone provider, but you just got denied getting a $300,000 mortgage to secure your home ownership dream. Let that sink in for a moment.

- if there is any “judgement” item on your report, be sure to solve it before having lender do a credit check on you. If you don’t, you better have a real good explanation to tell the lender what happened. “Judgement” and “collection” items are really eye sores that stick out in a very negative way. These could sometimes be show stopper items.

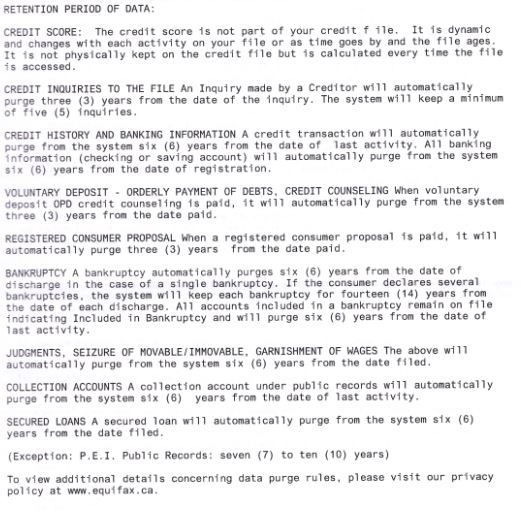

Below is direct statement from Equifax on how long they keep various items on your file like bankruptcy (6 -14 years), judgements (6 years), and collection accounts (6 years).

In my next Personal Finance Series # 3, I’ll talk about what you need to do to position yourself you to be eligible for largest mortgage amount possible. This needs to be done at least a couple months before having lender pull your credit and is incredibly important in such a tight lender environment. I see so many clients over the years going to lender and was shocked at how little they are qualified for even though they have good stable income.

Hope you find this information useful. Any questions, don’t hesitate to contact me. Until next time!

Gong Hay Fat Choy, Lay See Dow Loy!!

Disclaimer: We are not responsible for any errors or omissions in this article or blog. These are our personal opinions only.